There is currently press speculation that Labour Deputy Leader Angela Rayner failed to pay CGT on her house sale. Ms Rayner’s statement suggests she may have misunderstood the law. In some scenarios that could mean she failed to pay CGT of up to £3,500, but potentially less or zero. The amount of tax involved is therefore small but, in the interests of transparency, it would be helpful for Ms Rayner to clarify the position.

Here’s what appears to have happened, based on press reports and Angela Rayner’s statement:

- Angela Rayner bought her house on Vicarage Road in Stockport for £79,000 in January 2007.

- In September 2010, AR married Mark Rayner. At some point shortly before or after that date, AR moved into MR’s house.

- AR’s brother moved into her house from that time. AR didn’t charge him rent.1

- AR sold her property in March 2015 for £127,500. So a gain of £48,500 before we consider costs of acquisition/disposal (such as estate agent fees) and improvements such as extensions etc.

- MR’s property was sold in April 2016 for £145,250. We don’t know the purchase date or price.

- AR and MR separated in 2020

Ms Rayner says “As with the majority of ordinary people who sell their own homes, I was not liable for capital gains tax because it was my home and the only one I owned.”

This, however, isn’t how the rules work. Married couples2 can only have one principal residence for CGT purposes. A married couple who own more than one home are free to choose which is their “principal residence” for CGT purposes by sending a nomination to HMRC within two years of the situation arising.

I suspect many people would find every part of this surprising. Most taxation works by reference to individuals, so it’s odd this rule allows only one principal residence per married couple. Odder still that marriage potentially creates a big tax disadvantage. And even more curious that you are free to choose which property is your “principal residence” without reference to whether it really is. It’s therefore hard to blame Ms Rayner for misunderstanding the rules.

But it’s important to remember two things:

First, the tax system is complicated, and lots of people accidentally pay the wrong amount of tax (I’ve done it myself). That’s not a crime. It’s not a crime even if you’re careless or negligent. Ignorance is (in effect) a defence to the crime of tax evasion – because “tax evasion” means intentionally and dishonestly failing to pay tax. Calls for prosecutions for tax evasion were silly when we were talking about Nadhim Zahawi; they’re plain daft when we’re talking about Angela Rayner.

Second, everyone still has a duty to pay the correct amount of tax, and ignorance is no defence to having to pay it. Pay the wrong amount of tax (for any reason) and you’ll have to make up the difference, plus interest. And if you were careless, or fail to fess up to HMRC, then you’ll pay penalties too.

How much CGT is due

There are, broadly speaking,3 three possible scenarios:

1. AR and MR nominated AR’s house as their principal residence from 2010 to 2015

Again, it may seem weird that you can nominate somewhere as your principal residence when you don’t live there, but you can provided it’s been your home at some point, and you’re not renting it out. Letting someone live there for free is fine, and there’s no suggestion AR charged her brother rent.4

In this scenario then AR had no CGT to pay, but MR potentially had CGT on his 2016 sale – if there was a gain (we know nothing about whether there was or not).

2. AR and MR nominated MR’s house as their principal residence

AR still gets the principal residence relief for the three years before her marriage. She also automatically received principal residence relief for the last 18 months of her ownership.5

When the relief applies for part of a period of ownership, you make a simple pro-rata calculation. AR therefore is exempt for about 63% of the gain, and taxable for 37%.6

What’s the gain? It’s the £127,500 sale price less the £79,000 purchase price7, i.e. £48,500. AR should also deduct “allowable expenditure“. This will include estate agent, survey and conveyancing costs on the sale and purchase- I’d guesstimate all of this was around £4,000.8 There may also have been costs of improving the house, for example building an extension or conservatory – broadly speaking anything that adds value (but decorating doesn’t count). I’ll assume for the moment there were no improvement costs (that may be wrong given Ms Rayner’s reference to her brother being good at DIY).

So if we limit the allowable expenses to that £4k, the pro-rated gain would be £16k (£44,500 x 37%).

The CGT annual exemption amount for 2014/15 was £11,000. Meaning a taxable gain of about £5k and CGT of about £1.5k.9

And if AR had spent £15k or more on improvements, there would be no gain.10

So if we are in this scenario, and AR spent less than £15k on improvements, it may be that she accidentally failed to pay up to £1.5k of CGT. The rules are pretty complicated, with lots of special cases, so it would be wrong to assume this is the correct number. It is, however, probably the upper limit,11 and there are circumstances which could result in a smaller figure.

The other point about this scenario is that AR probably deserves more criticism: if she understood enough about the rules to make a nomination, then why didn’t she pay the correct amount of tax?

But it is of course also possible, and probably most likely, that she made no nomination at all.

3. AR and MR didn’t make a nomination

In that case the principal private residence relief applies by reference to the property that was AR and MR’s main residence as a matter of fact.

If AR moved in with MR from 2010 then that means the result will be the same as in scenario 2. If she moved in the year before, then she’d be exempt for about 48% of the gain rather than 63%. So more CGT to pay – about £3.5k rather than £1.5k.

Or the other way to view this is that, if she’d moved into MR’s house in 2009, AR would need to have spent £23k12 on improvements to have no capital gain.

The £3.5k figure is again probably an upper limit,13 and there are circumstances (aside from improvement expenditure) which could result in a smaller figure.

What next?

I’m not generally in favour of forcing politicians to publish all the details of their tax affairs – anyone with something to hide will hide it, and all we’ll see are prurient details of their financial affairs, plus the occasional accident/mistake. But now the story is out, it would be sensible for Ms Rayner to speak to a tax adviser and work out what her CGT position in 2015 actually was. If it turns out she failed to pay a small amount of CGT, I think most people would understand that as a mistake – but it’s a mistake she can and should explain and correct.

Credit to Politax for getting there first with this article; we both take a slightly different approach but end up in the same place.

Angela Rayner official photograph by David Woolfall, licensed under the Creative Commons Attribution 3.0 Unported license.

Footnotes

If that’s wrong then the position gets more complicated. Possibly more CGT. Possibly, because of the availability of letting relief, less/zero CGT (and letting relief probably doesn’t apply to informal arrangements where no rent is charged, although the point is not entirely clear). ↩︎

Who are living together – this is defined to basically mean “not separated”, so even if a married couple live separate lives in separate houses, they are probably “living together” for tax purposes ↩︎

Because they could have changed their nomination. ↩︎

Given the large gain that arises from buying a council house at a discount⚠️, nominating AR’s house may have been the rational move, even if it was slightly less valuable than MR’s house. ↩︎

The rules are now less generous – you only get nine months ↩︎

2,981 days of ownership, 1,339 days in which she lived there, 548 days for the last eighteen months. (1,339 + 548) / 2,981 = 63%). ↩︎

Probably! It is a bit of an unusual situation, because the purchase is plainly not at market value, thanks to the discount. CGT rules provide that, where a transaction is not at arm’s length (or between connected persons) then the actual value paid is replaced by the market value. One could argue that the unusual nature of a council house sale-at-a-discount, where the parties don’t negotiate at all, is that it’s not at arm’s length. If so, Ms Rayner would have £26,000 less gain, and so (after the pro-rata calculation and annual exemption) not tax to pay. However I am very doubtful that is the correct result. My instinct is that the council and Ms Rayner are unrelated parties, acting commercially, and the fact the sale terms are driven by statute doesn’t stop the sale being at arm’s length. However I have not researched the point and it may be more nuanced than this. Thanks to S for suggesting this point. ↩︎

I made some quick calls, and real estate contacts estimated that in 2015 the survey will have cost around £400, estate agent fees on her sale would have been about 1.5% plus VAT, plus conveyancing fees of about £600 on sale and purchase. ↩︎

Assuming AR had exhausted her basic rate band and so was taxed at 28%; also assuming AR had no other capital gains that year, and no carried-forward losses. These feel like reasonable assumptions. And finally, assuming that AR didn’t sell part of her interest in the property to MR before the sale, so using his annual exemption as well. That would likely have eliminated any CGT, but it’s the kind of planning that seems unlikely for someone who was not receiving tax advice at the time. ↩︎

I made a bad mistake in the original version of this article, and forgot that the improvement amount is subject to the same pro rata calculation as the gain. So I said £5k of improvements would mean no gain. My apologies – and many thanks to Martin Wardle on LinkedIn. It goes to show the danger of advising in an area where you don’t have real expertise. The original article was based on a discussion with three experts in this area, one of whom kindly reviewed the draft. However I added the “amount of improvements you’d need to eliminate the CGT” just before publishing, and didn’t check with the experts. So naturally that’s the bit I got wrong. It’s not good enough – my apologies. The practical difference means we’re probably now at the “new kitchen and bathroom plus other works” level of improvement required to zero the CGT, rather than just a new kitchen. ↩︎

Bearing in mind in this scenario we are assuming Ms Rayner lived in the house until she married ↩︎

The same bad mistake – the original version of this article said £12k ↩︎

Again noting the assumption that she moved out of Vicarage Road in 2009 ↩︎

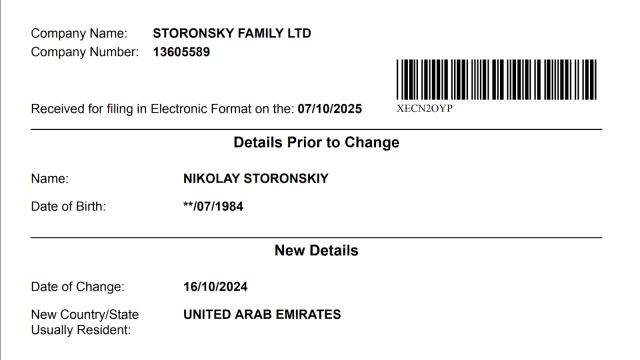

Could we have stopped Revolut’s founder from leaving the UK?

Will Labour tax your house sale? Why CGT on homes makes no sense

Are you living with your spouse? The unreal world of capital gains tax

The UK tax system favours capital gains. Is it an outlier?

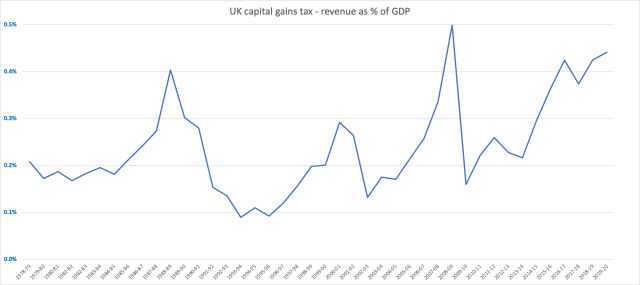

The history of UK capital gains tax in five charts

Leave a Reply to John Cancel reply