I have an exciting announcement. I’m setting up a tax consultancy called “Less Tax for Investors” and will be selling a brilliant way to escape inheritance tax on your ISA.1 To sign up as a client, please go here.

Our structure – which is approved by HMRC2 – is called the “hybrid partnership structure”. I’ll incorporate a limited liability partnership (LLP) and declare a trust over the ISA in favour of the LLP.34 And then, for the low low price of £25k, your ISA portfolio will qualify for business property relief (BPR) from inheritance tax.5

Your normal accountant won’t have told you about this because they’re not smart enough.

My marketing

I’ll go to investor events and run glitzy presentations, telling clients my structure means your ISA:

“is outside of your estate for inheritance tax, as long as you tick various boxes”

Why? Here comes the science bit:

“because the HMRC recognizes that there is a trading relationship between you all, and that you’ve got a written business plan and that you’re managing it and that your sole purpose is not to avoid tax but to maximize your wealth to tax efficiently as possible, the whole thing becomes inheritance tax free.”

Sometimes I’ll have a different explanation. But no need to worry, because HMRC agrees with me:

“The LLP structure that we set up is not investing in shares. It does not own the ISA. The ISA is owned by the individual. The LLP has taken advantage of that ownership and it is available… after two years, that LLP turns into a trading business according to HMRC, not according to us, according to HMRC. And at that point, after two years, the ISA inside that LLP is then outside of the estate for inheritance tax after two years. “

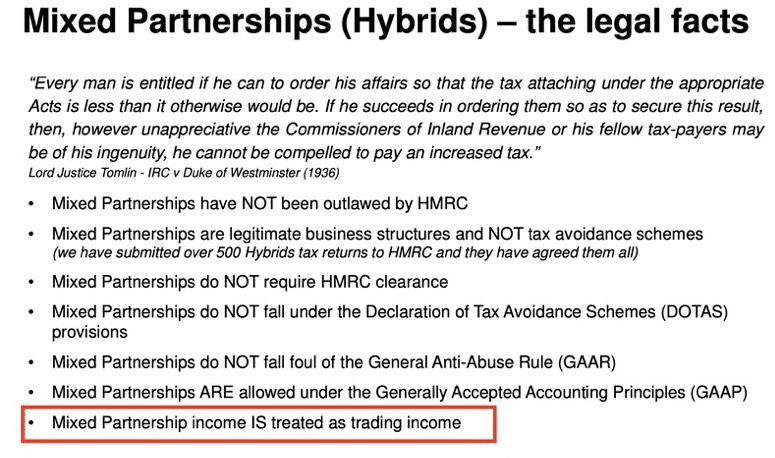

I’ll build a large team around me – accountants, salespeople, more salespeople. They’ll go around marketing my scheme using slides like this:6

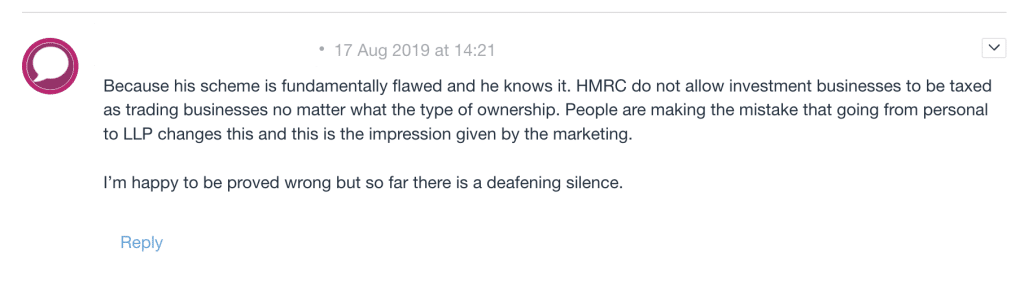

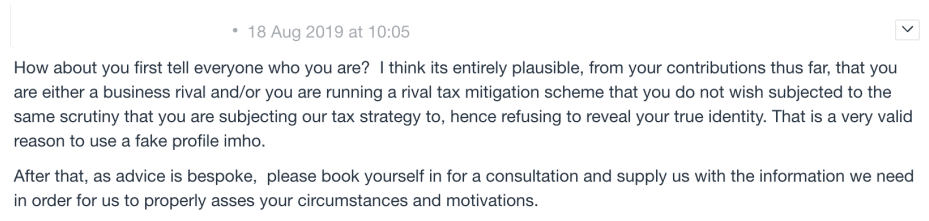

We’ll be frequently challenged by other advisers on internet forums:

We’ll respond aggressively, but never, ever, reveal why we think our scheme works:

When we receive more formal queries from clients’ existing tax advisers, we’ll give them nonsensical replies to make them go away:

“The LLP holds the equity and not the shares – so it cannot be classed as investment. The owner of the properties will not qualify for BR on the shares, but on the equity.“

I’ve another amazing idea – I’ll get clients to file tax returns on the basis they’re receiving a small amount of trading income through their LLP, and then claim this means HMRC has accepted the BPR position:7

What is true to say though is that we have had correspondence with HMRC where they have agreed that the partnership income received from the LLP is treated as trading income and as such, the clients pay the appropriate Class 2 and Class 4 National Insurance contributions.

And:

“Unfortunately, we have had clients die during the time that they have been clients and HMRC have accepted all of our probate calculations based on the above.“

Everything above is false. Do not do this, or anything like this.

You cannot make an ISA, or anything else, exempt from inheritance tax by holding it through an LLP.8

There is no technical basis for thinking this could work. It’s like claiming that you’re exempt from council tax if you paint your door pink. The structure does not work. The explanations are nonsense.

What will happen to Less Tax for Investors?

I can see the future, and it looks something like this:

- I’ll sell the scheme to hundreds of clients, making many tens of millions of pounds of fees, and avoiding £50m+ of tax.

- HMRC will eventually find out what I’m up to, warn taxpayers my scheme doesn’t work, and open enquiries into recent inheritance tax returns that used it.

- I’ll tell HMRC and my clients that I continue to believe the scheme worked. I’ll represent them in discussions with HMRC. I’ll pay a KC to come up with some arguments (any arguments!) that back up my position. This will go on for years.

- When this becomes indefensible, I’ll say that I genuinely thought the scheme worked. I was wrong, but tax law is complicated and HMRC is unpredictable. No, I won’t be refunding any fees. Sorry not sorry.

- Distraught family members who received a legacy under a Will will have large retrospective inheritance tax liabilities, plus interest and possibly penalties.

- Other clients will just have spent £20k+ on a complicated structure that doesn’t work, and will cost more money to unwind.

Can HMRC prosecute me for tax evasion? Or can the CPS prosecute me for defrauding clients?

It’s not a crime to get the law wrong. It’s not even a crime to get it recklessly wrong.9 The question is whether I was dishonest.10 That probably means in practice: did I take a position that either I knew was wrong, or was “wilfully blind” to the obvious possibility that it was wrong?

Nobody really knows if I was dishonest except me, and I’m not telling. But judges and juries don’t have to rely on confessions and psychics – they infer dishonesty from surrounding circumstances, and do so all the time. Here those circumstances would be:

- I am a tax lawyer. I’m not an inheritance tax specialist, but even a cursory look at the legislation or HMRC guidance would have made clear my scheme didn’t work.

- I was warned by advisers my scheme didn’t work.

- I gave nonsensical answers to the advisers.

- The critical point: I didn’t actually have any better answers. I had no technical basis for the position I took, even a bad one.

- I continued to sell my scheme, and made a lot of money from it.

Is it reasonable to infer from these facts that I was dishonest? Should I be prosecuted for defrauding HMRC and my own clients?

Less Tax for Landlords

The question above is not hypothetical. By a remarkable coincidence, my fictional scheme is very similar to the real scheme marketed by “Less Tax for Landlords”, which recently failed spectacularly:

- The concept is the same – take something that isn’t exempt from inheritance tax (a rental portfolio, an ISA portfolio) and claim that it becomes exempt when it’s owned through an LLP.

- Also the same: the lack of any apparent technical basis for the claim, and the nonsensical responses to advisers warning that there appeared to be no technical basis. One specialist inheritance tax KC we spoke to described the scheme as “mad and hopeless”.

- All the italicised quotes above are identical to those from Less Tax for Landlords (but with “property” replaced with “ISA”).11 The promotional slide is taken verbatim.

But there’s one important point we don’t know – did the critical line in bold above apply to Less Tax for Landlords? Did they, like hypothetical-me, have no technical basis for the position they took, even a bad one?

If they were just like hypothetical-me, then is it reasonable to infer from the known facts that some of those working for Less Tax for Landlords were dishonest and should be prosecuted for fraud/tax evasion?12

Or did they in fact have a proper technical justification, which they never revealed to anyone, and refuse to reveal now? And which is so brilliant or so obscure that not a single adviser we’ve spoken to has been able to guess it?

Or is there some other innocent explanation which they’re not telling, and our team hasn’t spotted?

I don’t know. But the question is important, and I’ll be writing more about it soon.

Thanks to M, L and P for their advice on the criminal law elements of this article.

Footnotes

This doesn’t work. None of this works. Do not do this. ↩︎

It isn’t ↩︎

The LLP has two members: the investor and a new company incorporated by the investor. ↩︎

Declaring a trust over a ISA is a very bad idea which will cause lots of problems. Do not do this. ↩︎

It won’t. No passive investment/share portfolio will qualify for BPR. ↩︎

The Duke of Westminster case hasn’t been good law for decades; any adviser citing it is waving a big banner saying “I don’t understand tax”. ↩︎

It doesn’t. HMRC is most unlikely to query whether the income is actually trading, but in no sense does that mean they’ve accepted the BPR position. ↩︎

Bizarrely you absolutely can make your ISA exempt from inheritance tax, by only holding AIM shares that qualify for exemption from business property relief. I am absolutely not recommending you do this, and it’s also not as simple as the previous sentence would suggest. ↩︎

The legal test for “dishonesty” has somewhat changed in recent years, although it’s unclear how much difference the change makes in practice. See this CPS summary. ↩︎

You can see those quotes here, some from their written materials and some from their promotional videos. ↩︎

To be clear, I am not saying they were dishonest – I’m saying that the absence of any apparent technical justification for the positions they took raises a real question as to whether any of those involved were acting fraudulently. I have given the principals at Less Tax for Landlords the opportunity to provide a justification or other explanation, and they have declined. Malcolm Rose and Tony Gimple deny fraud and say they acted in good faith. Chris Bailey, the only one of the team with accounting qualifications, has not commented. ↩︎

MP Estate Planning: the unregulated firm selling defective trusts to the elderly

![To: jeevacation@gmail com[eevacation@gmail com]

From: Peter Mandelson

Sem: Sun 11/7/2010 2 34 57 PM

Subyect: Fwd Rio apartment

Seat to mys bank manager Gratetul tor helpful thoughts trom my chief lite adviser

Sent from ims iPad

Bevin torwarded messave

From: Peter Mander iS

Date: 7 November 2010 [4 29 12 GMI

Subject: Rio apartment

P| ag awe dpeecussed Pan consdernne a purchase of an apartmentin Rion Ttisain](https://taxpolicy.org.uk/wp-content/uploads/2026/01/Screenshot-2026-01-31-at-21.27.15-640x360.png)

Emails show Peter Mandelson discussing Panama tax structure with Jeffrey Epstein

Tax barristers and fraud: how the Bar responded to our allegations

Rogue barristers are enabling a billion pound tax fraud – and the Bar won’t act

Samuel Leeds: the “property guru” and his bogus tax loopholes

Leave a Reply to Alun Cancel reply