In the last few months we may have given the impression that someone earning £50k, with three children under 18, faced a marginal tax rate of 68%. We may have suggested that this was a disincentive to work, contributed to a shortage of key workers and even held back economic growth. We may have used words like “indefensible” and “disgrace”.

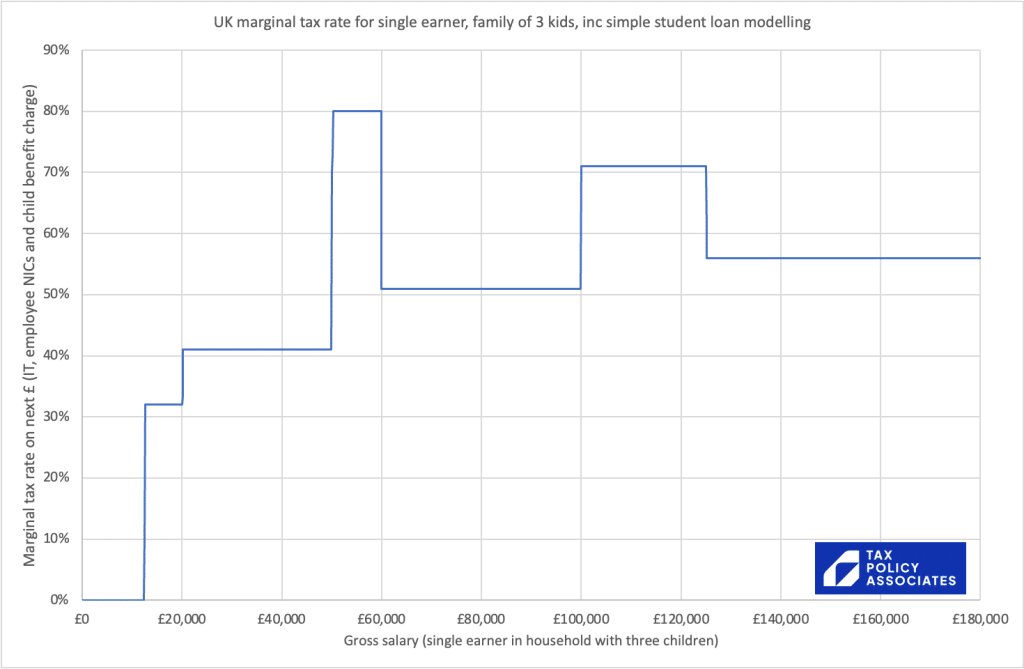

We now realise that our analysis failed to take into account the uprating of child benefit, and in fact the marginal rate in this scenario will be 71%, not 68%. A graduate in this position repaying a student loan can face a marginal rate of 80%.

We also wrongly suggested that someone earning £50k and with six children under 18 faced a marginal rate of 90%. The correct marginal rate is 96%.

We can only apologise for what is an unacceptable error, and would like to make clear for the record that a marginal rate of 71%, 80% or 96% is absolutely fine, and the effect on the individuals involved and the economy as a whole is completely unimportant.

The corrected chart showing the child benefit withdrawal/CBHIC effect:

And including student loan repayments:

The spreadsheet model is available here. Note these figures are for the UK excluding Scotland. The Scottish rates are higher.

The UK’s high marginal tax rates on people earning £50k are a disincentive to work. They’re made worse by the way a large chunk of the tax is collected – the “high income child benefit charge” (HICBC).

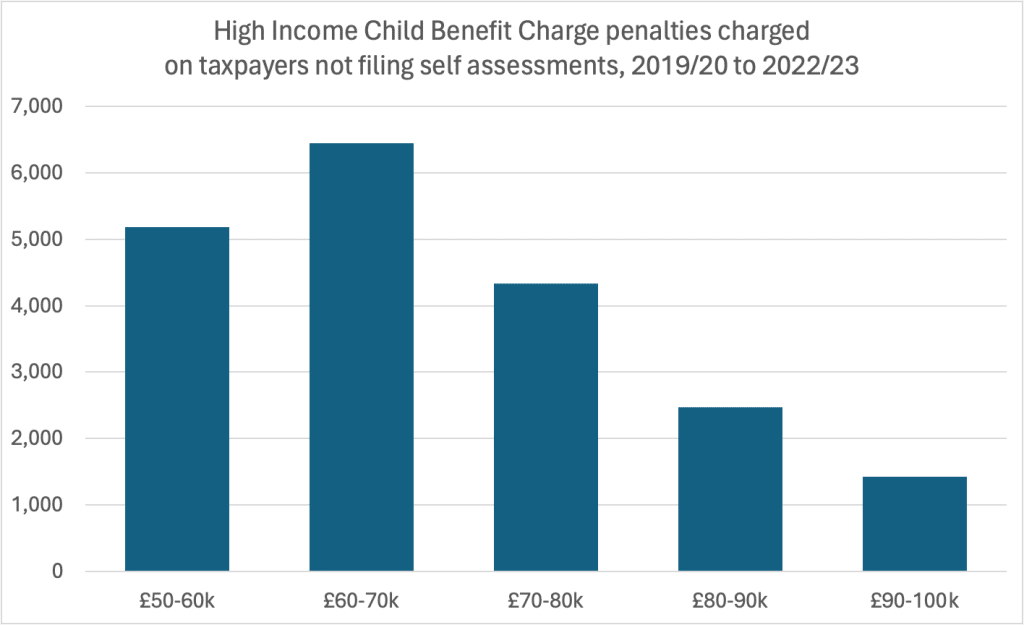

The HICBC creates a “tax trap” for employees who usually wouldn’t file a tax return. If they earn £50k, and they or their partner claims child benefit, they have an immediate requirement to file and pay the HICBC. It’s easy to get that wrong. In the last four years 19,000 did, and were hit with a penalty of up to 30%.

Tax systems shouldn’t have marginal rates of over 70%, and shouldn’t have “traps” that can catch the unwary. The HICBC should be abolished.

UPDATE: note that the income point where child benefit starts to be clawed back was moved from £50k to £60k in the Spring 2024 Budget. That’s an improvement – but all the problems of HICBC we discuss in this article stil remain.

The chart above shows the marginal rate of income tax paid by a UK taxpayer with three children under 18. That’s a 71% marginal tax rate between £50k and £60k.1

The high marginal rate results from George Osborne’s 2013 decision to withdraw child benefit from people earning a “high income” – £50,000. If the £50k threshold had been upgraded with inflation it would be £67,000 now – but it wasn’t. Around one in three households now include someone earning £50,000 – it’s not a “high income”.

How the HICBC works

Whatever we think of the politics of withdrawing child benefit from “high earners”, the way that it was done was a mess.

UK tax generally applies to individuals.2 I’m taxed on my income; my wife is taxed on hers. The benefits system on the other hand, looks at overall household income and capital. The decision was taken to withdraw child benefit based on a mixture of both – if the highest earner in a household hit £50,000 then child benefit would start to be clawed back, and if it hit £60,000 then all child benefit would be withdrawn.3

The challenge was that, whilst HMRC knows how much I earn, it doesn’t have a way to see how much the highest earning person in my household earns. So child benefit couldn’t “automatically” be clawed back.

The highly bureaucratic answer to this challenge was to outsource all the work to taxpayers. Osborne created a new tax – the HICBC – and required people to self-assess it in their tax return. It’s a bad answer because most people earning £50,000 are employees, and don’t file a tax return. So people would have to realise they had to start filing a tax return just because they claimed “too much” child benefit, and notify HMRC.

If your household has children under 18 and someone earning £50k, then you have three choices:

Don’t claim child benefit.

Register for child benefit but opt not to receive it.

Register for child benefit, receive it, and then pay some/all of it back through a special tax, the High Income Child Benefit Charge.

These are difficult choices with not-at-all-obvious outcomes:

The first choice – not claiming child benefit – seems the easiest thing to do, but is actually a mistake, because it means a non-working parent can lose their national insurance entitlement.4 It’s a mistake I made – and as a result my wife lost some pension entitlement. The Government pledged to fix this back in April, but nothing’s happened since.5

The second is the “correct” answer if the highest earner in a household makes £60k+ but not so great an answer if they earn £50-60k, because they’re then giving up all their child benefit unnecessarily.

The third is a pretty bad answer, but if the highest earner makes between £50k and £60k then it’s the only way to receive some child benefit. If you’re already on self assessment and filing online, then paying the HICBC is fairly easy – you just tick a box and type in the amount of child benefit claimed. But if, like most employed people, you’re not on self assessment, then you’ll have to register for self assessment. If you don’t, you’re breaking the law.

These choices all get more complicated if income unexpectedly changes during a year, or a couple separate, or a couple move in together.

And lots of people get it wrong. Sometimes in the Dan’s-wife-loses-some-of-her-pension way. And sometimes in failing to realise you now have to register for self assessment and file/pay the HICBC.

How many people get it wrong?

Almost 20,000 people who weren’t on self assessment were hit with penalties from 2019/2020 to 2022/23 for not realising6 they should be paying the HICBC:7

We don’t have data on the amount of the penalties, but likely it was several hundred pounds.8

This is after an HMRC review of HICBC penalties in 2018 – before then, there were about twice as many penalties issued.9

HMRC has sent millions of letters to people warning them about the HICBC, but not everyone affected has received one. HMRC has pursued people for penalties even when they weren’t adequately informed; tax tribunals have been reasonablysympathetic to taxpayers.10

What should happen?

Marginal rates of over 60% should be regarded as unacceptable. I’d abolish the HICBC on this ground alone.

But the way the HICBC was implemented is an illustration of how a tax system shouldn’t work. A wholly disproportionate level of complication for people on not-very-high incomes doing something as ordinary as having children, where the total amount of tax at stake is so small (likely around £1bn).

The Government has promised to improve things by enabling HICBC to be collected through PAYE, removing the need to file a self assessment form. But taxpayers would still have to notify HMRC this, and still have to make surprisingly difficult choice as to how to proceed.

I’d hope abolishing the HICBC would appeal to both a Conservative Party that regards high marginal rates as an anathema, and a Labour Party that’s always supported the principle of universal child benefit. The amount of money at stake is small, and if the government wished to recoup the cost from people earning £50k, that could be easily done in a less damaging way (for example by upgrading the higher rate income tax threshold slightly more slowly than it otherwise would).

There are a number of cases where it’s more complicated than this. For example: where the high earning parent doesn’t know if the other parent claims child benefit, or where child benefit is claimed by someone outside the household but who provides the household with financial support. I’m going to ignore these issues for now, but they’re important for the people affected. ↩︎

It also means the child won’t automatically receive a national insurance number when they turn 16 ↩︎

Thanks to Miro in the comments for reminding me of this. ↩︎

My assumption is that it was almost always an accident, because I think it would be obvious to most people who understood the system that they would be caught ↩︎